Looking for Mispriced Opportunities in a Chaotic Market

The global equity markets have recently experienced a significant period of volatility, shaped by a mix of macroeconomic developments and policy shifts. The sell-off in the S&P 500 was driven mostly by tariff-related concerns, though it managed a partial recovery toward the end of the quarter. Concerns around economic growth intensified, fueled by softer economic data and uncertainty surrounding the broader “Trump 2.0” policy framework. Survey data reflected this caution, as the March Michigan Consumer Sentiment Index fell to its lowest since November 2022, with one-year inflation expectations rising to 5% and five-year expectations hitting a 32-year high of 4.1%. The March Consumer Confidence Index also dropped to its lowest since January 2021, with the expectation component reaching a 12-year low. Manufacturing PMI swung back into contraction, with cost pressure rising at the sharpest pace in 23 months.

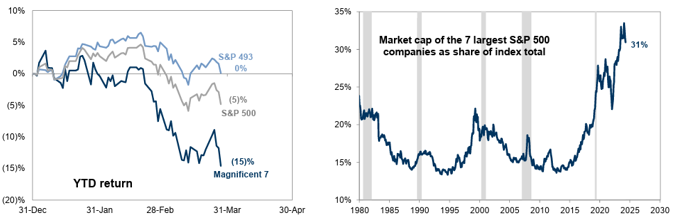

All in, the S&P 500 declined -4.59% in 1Q25, which marked its weakest performance since 3Q22. The best-performing sectors were Energy (+9.30%), Healthcare (+6.08%) and Consumer Staples. Conversely, sectors that underperformed were Industrials (0.53%), Communication Services (-6.41%), and Technology (-12.79%).

High single-stock concentration levels in the S&P 500 Index, Deep Seek Artificial Intelligence developments, and elevated valuation multiples resulted in the Magnificent Seven stocks underperforming the broader market. In fact, the Magnificent Seven collectively fell into bear market territory, as the group declined -15% during 1Q25 and is now down -20% since the peak in December 2024.

Source: Goldman Sachs

Another overhang was the Federal Reserve’s Summary of Economic Projections (SEP) that lowered the median 2025 US GDP growth rate by -40 basis points to +1.7%, along with the median core PCE inflation forecast being revised upward by +30 basis points to +2.8%. On a more positive note, the US labor market remains healthy, as exhibited by the March Employment report, which cited an unemployment rate of 4.2%.

Outlook:

According to FactSet, Wall Street bottom-up S&P 500 EPS estimates for 1Q25 have declined by -3.8% since the start of the quarter, reflecting uncertainty from the impact of tariff policies and weakening consumer confidence. With the prospect of potential further downward earnings revisions, we believe owning businesses with undemanding valuations, strong pricing power, variable cost structures, cost removal initiatives, and high barriers to entry should perform well in a challenging macro-economic backdrop.

Looking ahead, global trade dynamics will remain a key factor influencing markets. Corporate earnings will offer insights into how businesses manage cost pressures and consumer demand (tarriff impacts). Macroeconomic indicators, including inflation trends and Federal Reserve policy, will also shape investor confidence.

Despite these issues, we remain focused on identifying businesses that are trading below their intrinsic value and offer compelling opportunities in the long run. At Oliver Luxxe, we believe our “Private Equity in the Public Marketplace” investment framework allows us to identify businesses that have strong balance sheets, sustainable cash flow generation, and compelling reinvestment opportunities. We are utilizing the current market volatility and uncertainty in an effort to improve the quality of our clients’ portfolios over the next three to five years.

As always please reach out with any questions or concerns.

Thank you,

Joseph Sharma, CFA

Chief Investment Officer

Direct: (908) 741-8340

Disclaimer

Investments in securities entail risk and are not suitable for all investors. This is not a recommendation nor an offer to sell (or solicitation of an offer to buy) securities in the United States or in any other jurisdiction. All investment strategies have the potential for profit or loss; changes in investment strategies may materially alter the performance and results of a portfolio. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client’s investment portfolio.

This document may contain forward-looking statements relating to the objectives, opportunities, and the future performance of the US market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to the success or lack of success of any particular investment strategy. All are subject to various factors, including, to general and local economic conditions, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of Oliver Luxxe or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.