“Those who have knowledge don’t predict. Those who predict don’t have knowledge.”

- Lao Tzu

The first quarter of 2026 proved to be a turbulent period for financial markets. What began as a muted but broadly resilient market environment was upended in late February by the launch of Operation “Epic Fury”. The resulting energy supply shock and repricing of Federal Reserve rate expectations both led to meaningful cross-asset volatility. Major U.S. equity indices finished the quarter mostly lower. Prior to the outbreak of conflict with Iran on February 28th, markets were broadly positive, as the Russell 2000 was up +6.20%, the S&P 500 had gained +0.67%, and the Nasdaq was down -1.33%. The subsequent escalation reversed those moves and weighed on returns through quarter-end, with the S&P 500 finishing down -4.63%, the Dow down -3.58%, and the Nasdaq declining -7.11%. The notable exception was the Small-Cap Russell 2000, which edged higher by +0.58%.

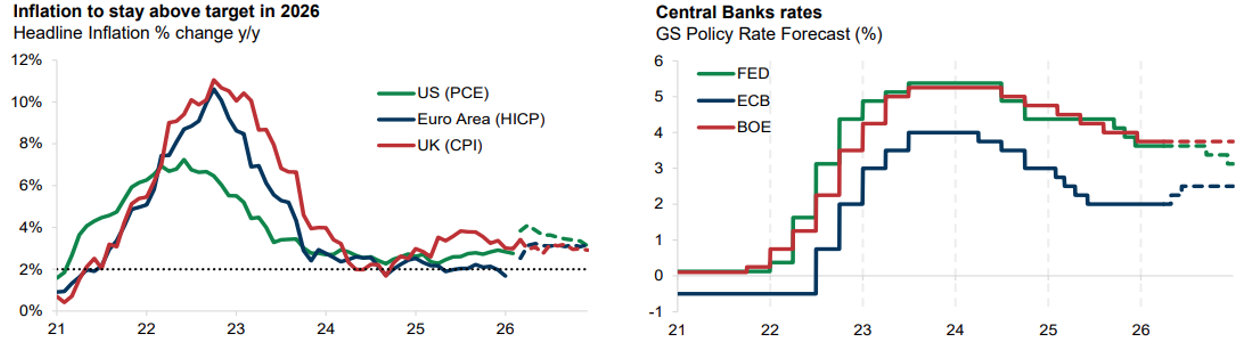

The Federal Reserve entered 2026 with a policy rate in the range of 3.50% to 3.75%, having cut rates a cumulative 175 basis points since September 2024. As recently as late February, bond markets were still pricing in more than 50 basis points of additional easing before year-end 2026. That expectation was reduced by quarter’s end, driven by a combination of potentially higher inflation, a geopolitically induced energy shock, and growing concern that the Fed’s hands were tied by competing pressures on its dual mandate.

The U.S. labor market spent 1Q26 in what the Stanford Institute for Economic Policy Research described as a “low-hire, low-fire equilibrium”. Layoffs remained historically low, and the unemployment rate held near the full-employment level economists generally associate with the natural rate (i.e., around 4.0% to 4.1%). However, gross hiring activity remained subdued, and payroll growth was narrowly concentrated in just a few sectors, leaving the headline numbers more fragile than their surface stability suggested.

The U.S. economy entered 2026 with sustained momentum, as Real GDP grew at a 4.4% annualized rate in Q3 2025 and an estimated 2.0% in 4Q25. The 4Q25 slowdown partly attributable to the government shutdown that disrupted federal activity in October. Full-year 2025 growth came in at approximately 2.0%, consistent with or slightly above long-run trend, a notably solid result given the cumulative headwinds from elevated interest rates and policy uncertainty. Business investment was another constructive driver of GDP growth, as AI-related capital expenditures accounted for a disproportionate share of non-residential investment in 2025. However, the return on investment (ROI) debate around these outlays has generated ongoing scrutiny from investors.

Outlook

Despite the volatility seen during the first quarter, the underlying U.S. economy remains on reasonably solid footing. Consumer spending has held up, GDP growth is tracking near potential, and the broader economic expansion shows few signs of rolling over. The resilience is notable given the cumulative weight of elevated interest rates and geopolitical uncertainty.

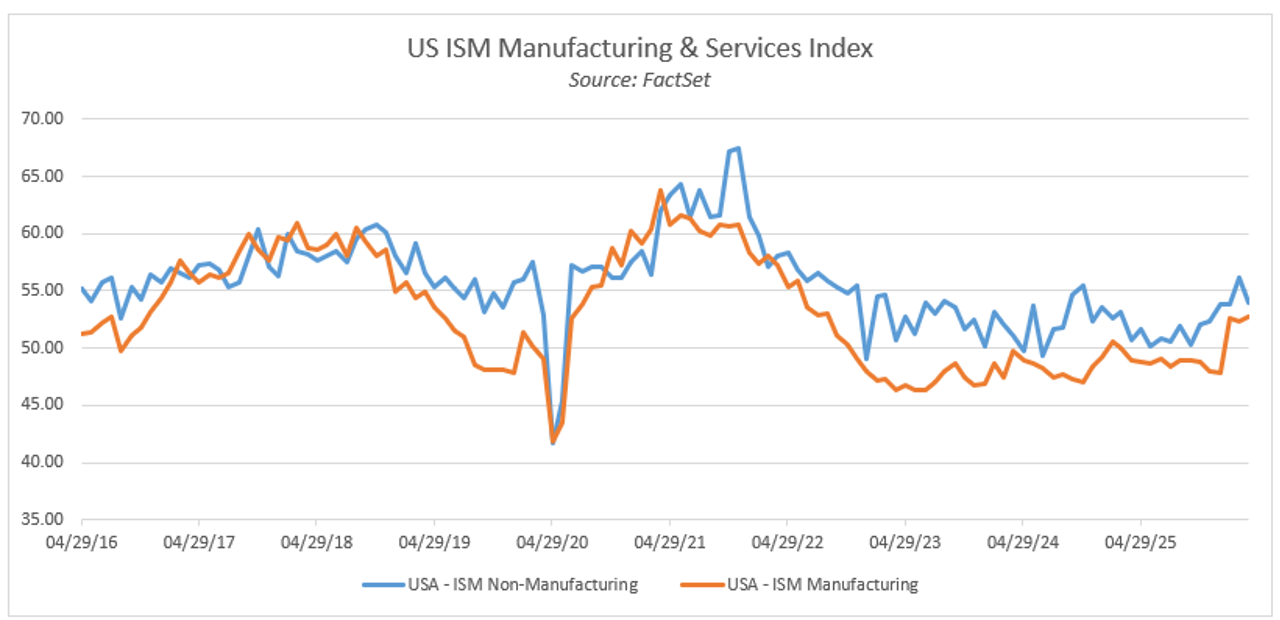

One encouraging development is the nascent recovery in the manufacturing sector. The US ISM Manufacturing Index has now inflected positively for three consecutive months. This is a streak that has historically signaled a broadening of economic activity beyond the consumer and services sectors. The labor market, while cooling at the margin, remains stable. Layoffs are not elevated, the unemployment rate is holding near full-employment levels, and wage growth continues to support household purchasing power. The hiring environment is cautious, but there is little in the current data to suggest a material deterioration is imminent.

Taken together, the economic backdrop for the remainder of 2026 is more constructive than recent market volatility might imply. The primary risk remains the duration and resolution of the Iran conflict and its inflationary effects. However, absent a significant further escalation, the foundation for a continued, modest expansion for the US economy appears intact. At Oliver Luxxe, our "Private Equity in the Public Marketplace" investment philosophy is driven by identifying businesses with durable balance sheets, consistent cash flow generation, and attractive opportunities to reinvest capital for long-term growth. Across our equity strategies, we view market volatility as an opportunity rather than a risk. Periods of uncertainty allow us to upgrade portfolio quality and add to high-conviction positions at more attractive valuations.

As always, please feel free to reach out to us if you have any questions. Thank you.

The Oliver Luxxe Assets Team

Matt Biedron, CFA, Interim CIO

Brad Jacobson, Managing Director

Drew Crawford, Jr., Director of Research

Eric Feigenwinter, Research Associate

Disclaimer

Investments in securities entail risk and are not suitable for all investors. This is not a recommendation nor an offer to sell (or solicitation of an offer to buy) securities in the United States or in any other jurisdiction. All investment strategies have the potential for profit or loss; changes in investment strategies may materially alter the performance and results of a portfolio. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client’s investment portfolio.

This document may contain forward-looking statements relating to the objectives, opportunities, and the future performance of the US market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to the success or lack of success of any particular investment strategy. All are subject to various factors, including, to general and local economic conditions, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of Oliver Luxxe or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.