Fourth Quarter 2025 Quarterly Market Recap & 2026 Outlook

The fourth quarter of 2025 capped off a resilient year for U.S. equities, with major indices posting positive returns amid moderating economic growth, persistent inflation pressures, and a cautious Federal Reserve. The S&P 500 advanced approximately 2.7% in Q4, contributing to a full-year gain of around 18%, driven largely by technology, AI, and communication services sectors. This represents the third consecutive year of double-digit gains.

Despite headwinds from policy uncertainty and a projected economic slowdown, markets climbed a "wall of worry," with investors rebalancing portfolios and corporate optimism supporting rallies. Key risks heading into 2026 include potential policy shifts, below-trend GDP growth, and inflation drifting above the Fed's target.

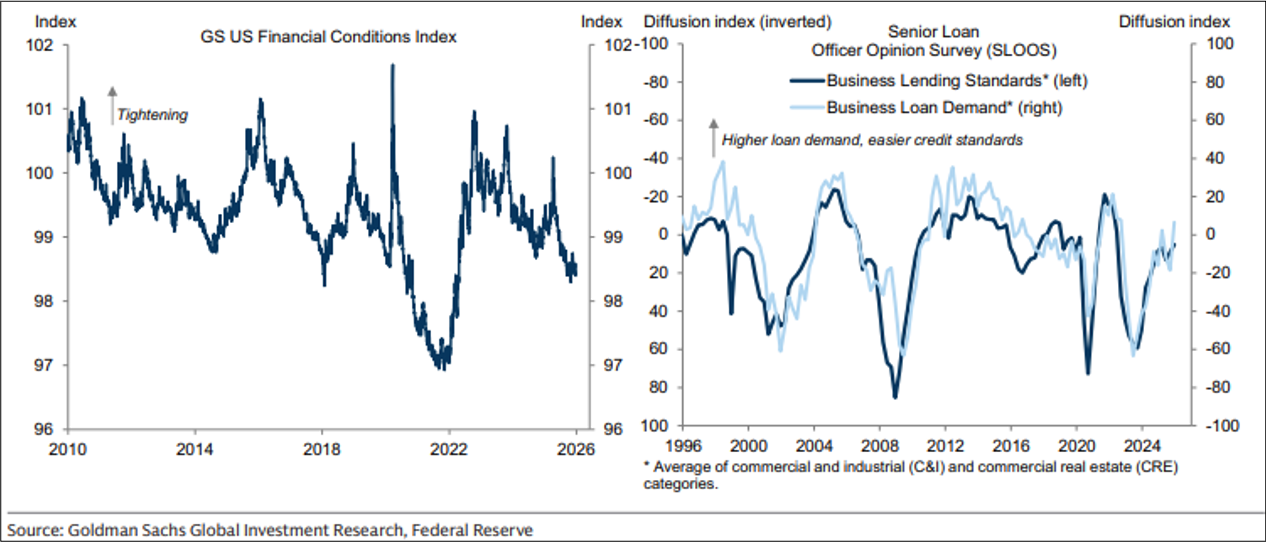

As we enter 2026, we believe the global economy should transition to a period of improved economic stability as the path of global trade become clearer. We believe the US equity market should experience measured progress amid a resilient yet evolving economic landscape. In 2026, US equity returns should be driven by fundamentals, particularly earnings growth, rather than further valuation multiple expansion, as current multiples are already above long-term averages. Importantly, corporate profit margins are set to improve in 2026, as companies benefit from operational efficiencies, AI productivity gains (albeit on low adoption rates), and moderating input costs. Additionally, financial conditions are expected to become easier than in early 2025 (see charts below).

Inflation is forecasted to continue its downward path in 2026, easing from elevated levels in 2025 toward the Federal Reserve's 2% target, though it may remain sticky due to wage pressures and tariff effects. The largest component of the US CPI Index: shelter, which comprises about 40% of the index and includes owners’ equivalent rent, is expected to decline in 2026 (see chart below).

This downward trajectory should allow the Federal Reserve to continue its gradual rate cuts, potentially bringing the target range towards 3.25% by mid-year, allowing for a more accommodative environment for risk assets. The US labor market is expected to weaken modestly in 2026, with unemployment rising and hiring slowing, reflecting a cooling from the tight conditions of prior years.

US economic growth is expected to remain solid in 2026, reflecting a resilient economy that avoids recession despite headwinds from tariffs and fiscal policy adjustments. Additionally, economic growth in 2026 is anticipated to broaden beyond the technology and AI-driven sectors, with increased contributions from cyclical areas such as manufacturing, materials, energy, and industrials, buoyed by infrastructure spending and easing monetary policy. This broadening should reduce market concentration risks (i.e., Information Technology) and support more diversified equity performance, including small and mid-cap cyclical sectors of the economy.

As 2026 unfolds, we remain focused on identifying businesses that are trading below their intrinsic value and offer compelling investment opportunities in the long run. At Oliver Luxxe, we believe our “Private Equity in the Public Marketplace” investment framework allows us to identify businesses that have strong balance sheets, sustainable cash flow generation and compelling reinvestment opportunities. We will seek to utilize market volatility and uncertainty to improve the quality of our clients’ portfolios over the next three to five years.

As always please reach out with any questions or concerns.

Thank you,

Joseph Sharma, CFA

Chief Investment Officer

Direct: (908) 741-8340

Disclaimer

Investments in securities entail risk and are not suitable for all investors. This is not a recommendation nor an offer to sell (or solicitation of an offer to buy) securities in the United States or in any other jurisdiction. All investment strategies have the potential for profit or loss; changes in investment strategies may materially alter the performance and results of a portfolio. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client’s investment portfolio.

This document may contain forward-looking statements relating to the objectives, opportunities, and the future performance of the US market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to the success or lack of success of any particular investment strategy. All are subject to various factors, including, to general and local economic conditions, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involve a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of Oliver Luxxe or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made.